Address newsletter

Get the latest news on buying, selling, renting, home design, and more.

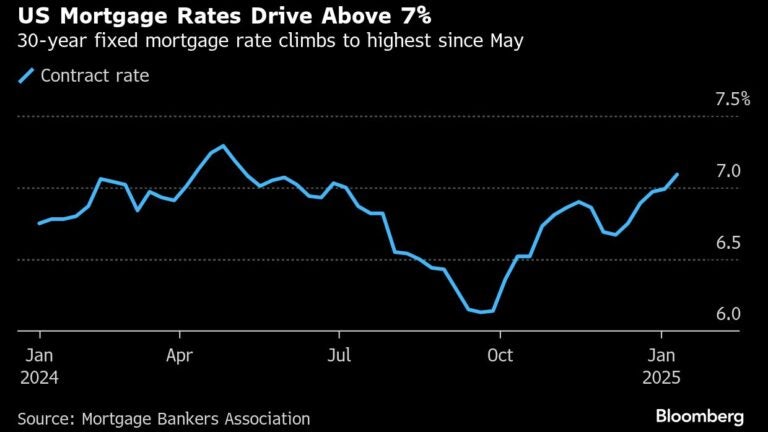

The average rate on a 30-year mortgage in the United States ticked up this week to slightly above 7 percent, the highest level in eight months.

The rate rose to 7.04 percent from 6.93 percent last week, mortgage buyer Freddie Mac said Thursday. It has risen for five straight weeks. A year ago, it averaged 6.6 percent. Five years ago, it was 3.65 percent, according to the Federal Reserve Bank of St. Louis.

The elevated mortgage rates, which can add hundreds of dollars a month in costs for borrowers, have discouraged home shoppers, prolonging a national home sales slump that began in 2022.

Here’s a look at how much elevated mortgage rates can affect a home buyer’s purchasing power. These calculations are based on a 30-year fixed mortgage on a $500,000 loan with no down payment:

| DATE | MORTGAGE RATE | MONTHLY PAYMENT |

INTEREST OVER LIFE OF 30-YEAR LOAN |

|---|---|---|---|

| 1/16/2020 | 3.65% | $2,287.30 | $323,427.21 |

| 1/9/2025 | 6.93% | $3,303.04 | $689,094.36 |

| 1/16/2025 | 7.04% | $3,339.96 | $702,383.88 |

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners seeking to refinance their home loan to a lower rate, also rose this week. The average rate increased to 6.27 percent from 6.14 percent last week. A year ago, it averaged 5.76 percent, Freddie Mac said. Five year ago, it stood at 3.09 percent, according to the Federal Reserve Bank of St. Louis.

The uptick in the cost of home loans reflects a rise in the bond yields that lenders use as a guide to price mortgages, specifically the yield on the U.S. 10-year Treasury. The yield on the 10-year Treasury has climbed from 3.62 percent in mid-September to 4.61 percent as of midday Thursday.

Get the latest news on buying, selling, renting, home design, and more.

To comment, please create a screen name in your profile

To comment, please verify your email address

Conversation

This discussion has ended. Please join elsewhere on Boston.com