Address newsletter

Get the latest news on buying, selling, renting, home design, and more.

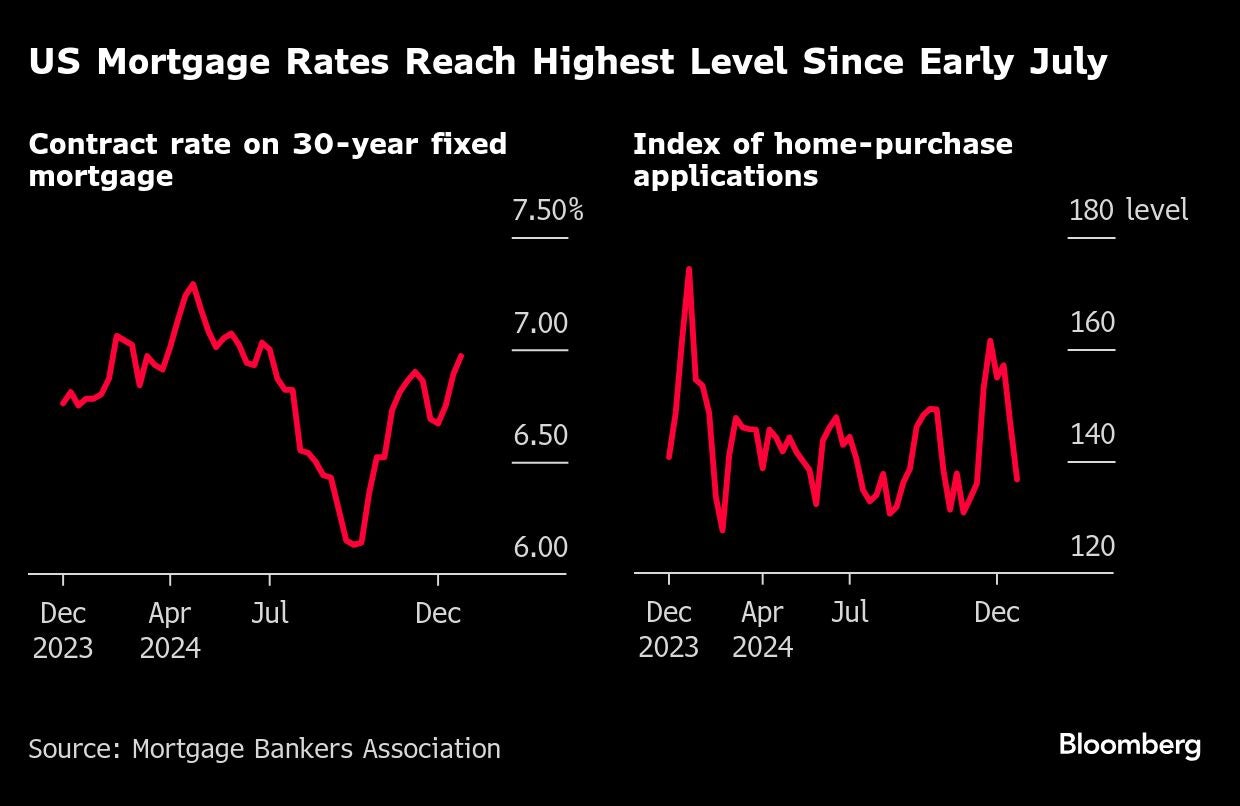

WASHINGTON (AP) — US mortgage rates rose this week to the highest level since July.

The benchmark 30-year fixed rate loan rate rose to 6.91 percent from 6.85 percent last week, according to mortgage giant Freddie Mac. It was at 6.62 percent a year ago, and it was 3.72 percent five years ago, according to the Federal Reserve Bank of St. Louis.

The uptick in the cost of home loans reflects a rise in the bond yields that lenders use as a guide to price mortgages. The increase is occurring with the price of homes rising steadily.

The average rate on a 15-year fixed-rate mortgage, popular with homeowners seeking to refinance, climbed to 6.13 percent, up from 6 percent and also the highest since July. It was at 5.89 percent a year ago, and 3.16 percent five years ago, according to the Federal Reserve Bank.

“Inching up to just shy of 7 percent, mortgage rates reached their highest point in nearly six months,” said Freddie Mac chief economist Sam Khater. “Compared to this time last year, rates are elevated and the market’s affordability headwinds persist. However, buyers appear to be more inclined to get off the sidelines as pending home sales rise.”

Interest rates have been climbing since the Federal Reserve signaled last month that it expects to raise its benchmark rate just twice this year, down from the four cuts it forecast in September.

The reason the Fed is tapping the brakes is that inflation remains stubbornly above the central bank’s 2 percent target, even though it’s fallen from the heights it reached in mid-2022. Economists also worry that President-elect Donald Trump’s economic policies, notably his plan to vastly increase tariffs on imports, could fuel inflation.

Get the latest news on buying, selling, renting, home design, and more.

To comment, please create a screen name in your profile

To comment, please verify your email address

Conversation

This discussion has ended. Please join elsewhere on Boston.com