Newsletter Signup

Stay up to date on all the latest news from Boston.com

A Boston Indicators report finds that Black and Hispanic residents in Massachusetts are saving far less money for retirement than their white counterparts, perpetuating wealth gaps in the state and across the U.S.

The report, done in collaboration between the Boston Foundation and the Federal Reserve Bank of Boston, finds racial differences in both accessing retirement funds and the amounts of retirement assets saved.

“In recent years, civic leaders in the Greater Boston region have come to recognize racial wealth inequality as one of the biggest challenges we face,” said Luc Schuster, senior director at Boston Indicators.

But, he said, the conversation around the levers to address the problem overlooks the importance of retirement savings. The focus is often on boosting homeownership in communities of color or boosting small business development and entrepreneurship.

“But when you look at the data … you see that retirement makes up a much bigger piece of the wealth puzzle than I think many people appreciate,” Schuster said.

For families approaching retirement age, Schuster said, those between 40 and 65, middle-class families, and especially Black families, retirement is the largest source of wealth.

The report finds that Social Security benefits are the largest source of retirement income for older Americans, providing a monthly inflation-adjusted benefit over post-retirement life. However, the report looked solely at private wealth disparities.

Schuster said that including defined benefit pensions helps close racial wealth gaps between Black and white families a bit: “Certainly far from totally closing the gap.”

Public sector union jobs are among the few pathways Black families have in the U.S. to the middle class. They are also one of the few segments of the economy that still offer defined benefit pensions.

“The really alarmingly low levels of Black wealth that people see from some other data sources still are low when you include defined benefit pensions, but not quite as low as those estimates,” Schuster said. But “there are still enormous racial gaps.”

In Massachusetts, there are also very large gaps for Hispanic workers with low levels of defined benefit pensions, 401(k) assets, and Individual Retirement Accounts (IRA).

“We are 14% of the state’s population, and the retirement wealth gap is a significant concern,” said Roxanna Sarmiento, the director of marketing and communications for the advocacy group Amplify LatinX. “Much of what we hear is about the workforce leaving Massachusetts because it’s so expensive. But Latinos are staying.”

Sarmiento said many of those Latinos are building businesses and are micro-business owners. But she said it is very hard for small businesses to offer 401(k) plans to their employees, let alone to themselves.

For many Latinos, the joke is, “We are our parents’ retirement plan,” Sarmiento said.

Many Latinos are children of immigrants who, during their working years, establish themselves, survive, and work in small businesses that don’t offer retirement plans, Sarmiento said. So, for many working-age Latinos in the state, they are not only supporting their children but also their parents, she said.

Many Latinos are also disproportionally represented in industries such as construction and the service sector that don’t have the same advantages, such as retirement savings, that white-collar jobs have.

About 60% of white workers nationally have access to defined contribution plans like 401(k) and defined benefit plans like pensions through their jobs, compared to 52% of Black employees and 44% of Hispanic workers.

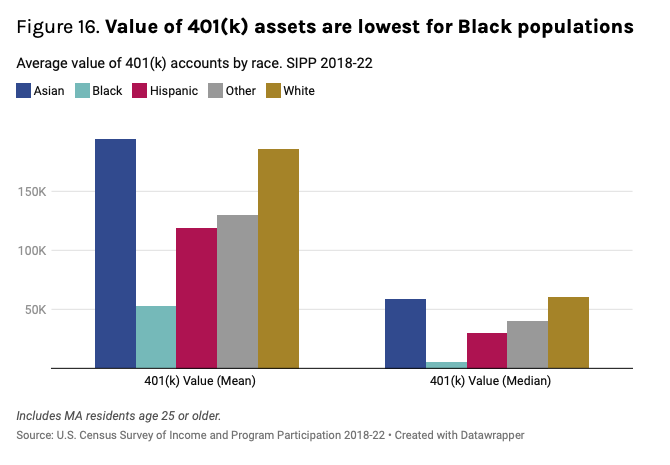

Of those who do have access, the report found that between 2018 and 2022, the median value of white residents’ 401(K) was about $60,000, while Hispanics’ was about $30,000 and Blacks’ around $5,000.

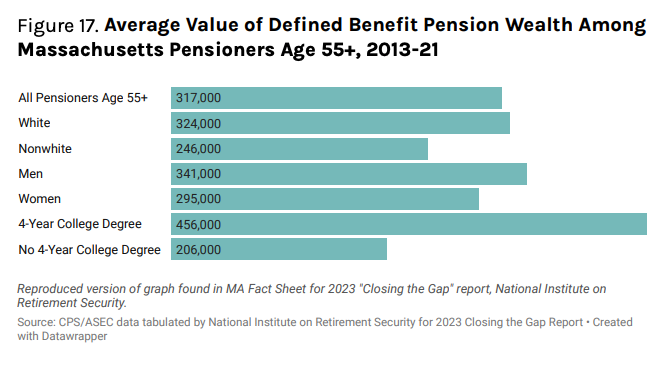

Even though pensions are becoming less common, the disparities between races, genders, and education levels remain.

The average value of Massachusetts employees with defined benefit pensions shows white residents at $324,000 compared to nonwhite residents at $246,000. The report also showed disparities between men, at $341,000, and women, at $295,000, and between those with a four-year college degree, at $456,000, and those without, at $206,000.

Even though white and Asian workers in the state hold substantially greater 401(k) assets than their Black peers, the gaps are less evident in public sector workers. Black workers in the state are more likely than their white and Hispanic peers to be employed in public sector jobs that offer high-quality pensions. The only exception is teachers; the report found Black workers to be underrepresented.

“That makes sense because retirement in the United States is so tied to your job,” said Schuster. “So lower wage service sector workers are far less likely to have a strong, generous retirement plan offered by their employer.”

He added that it is much harder for economically insecure people to commit some of their income to longer-term savings during their working years.

Many workers also opt out of plans with little or no employer-matching contributions. Others cannot make ends meet or are holding debt they prioritize over contributing to a retirement account. Younger workers may wait until later in life to start saving.

The report found that white workers participate in retirement savings accounts more. In the public sector, 87% of whites are covered compared to 75% of those of color; 61% of white workers in the private sector participate in an employer-sponsored plan, and only 46% of workers of color do.

The report highlights a few possible policy changes to close the gap.

In Massachusetts, a proposed IRA-style plan called Secure Choice would provide opportunities for employees who do not have access to an employer-based plan.

Other options include ensuring that all workers understand their options, enhancing the ability to move over retirement plans from previous employers, and setting up automatic enrollment, which the report finds makes it 20 times more likely that employees will save.

“I can only imagine the strain on the state’s economy as people get older and retire,” said Sarmiento. “This is the time to tackle this.”

Stay up to date on all the latest news from Boston.com

To comment, please create a screen name in your profile

To comment, please verify your email address

Conversation

This discussion has ended. Please join elsewhere on Boston.com